Benchmarking Methodology:

The methodology of the DataBeat’s Programmatic Trends Report for January 2024 lies on the analysis of anonymized data, sourced from some of the industry partners within the databeat network.

In this report, we compared Jan 2024 performance to Dec 2023 performance for programmatic advertising demand in the United States. As everyone in the industry is aware, the lowest CPMs are typically obtained at the beginning of January each year.

Key Highlights:

This month, the overall CPM experienced a significant drop of nearly 30%, with Display down by 39% and Video following closely with a 31% decrease. This trend is in line with expectations for the beginning of the year.

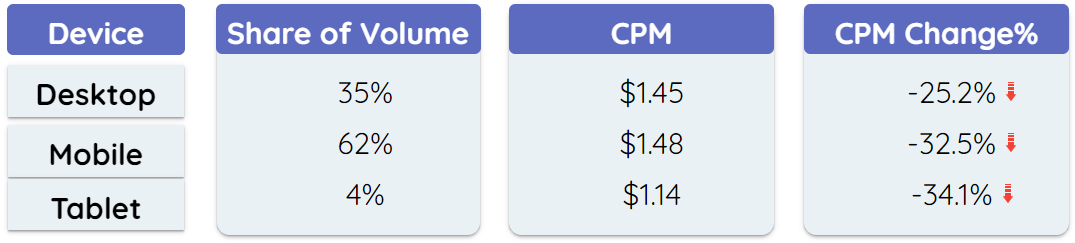

Device Trends:

- While mobile devices continue to dominate the industry with a substantial 60% share of volume, it is noteworthy that they also exhibit the highest drop in CPM, experiencing a 32% decline.

- In contrast, desktops, with a lower CPM drop of 25%, show a more resilient performance. Interestingly, the CPM gap between desktop and mobile is minimal, suggesting that advertisers are allocating similar budgets for both desktop and mobile ad formats.

- Though tablets hold a smaller share of volume, over the last few months, they have performed very consistently due to the unique blend of behavior inherited from both desktop and mobile platforms.

Programmatic Integrations Trends:

In the programmatic landscape, client-side prebid integration stands out as the most widely recognized and utilized method among web publishers. Virtually every SSP supports this integration, resulting in prebid’s share of volume being 38% higher than any other integration within the programmatic ecosystem.

- As the market leader, Google, despite seeing a 30% drop in CPM, maintains a substantial share of volume, solidifying its position as a formidable competitor and essentially operating as a monopoly in the industry.

- TAM CPMs dropped by 24% but still able to compete with Google and Prebid in taking consistent share of volume from the publisher’s inventory.

- While EBDA may be a smaller player in the industry, it has been significantly influenced by the Google trends, The shifts in Google’s demands play a pivotal role in shaping the EBDA performance.

Prebid Top SSPs Highlights:

- Rubicon has the highest volume share of client-side prebid integration, which could be attributed to the fact that they also offer prebid wrapper solutions to their publishers.

- Despite Microsoft Bing’s shift from TripleLift to Appnexus, TripleLift maintains a strong position in the Top 3, holding over 10% share of volume with a mild 10% drop in CPM.

- Media.net and YieldMo witnessed the highest CPM drops of more than 40% among the top ten prebid ssps.

TAM Top SSPs Highlights:

- Since TAM is owned by Amazon, a large chunk of inventory is taken by Amazon accounting for 28% of share of volume, and their CPM dropped by 28% which aligns with big players in the industry like Google, Rubicon.

- Unlike in prebid integration, TripleLift experienced a significant drop in CPMs by nearly 25% in TAM, and despite this, TripleLift still stands second among TAM’s top SSPs.

- A complete contrast trend has been observed from YieldMo in TAM, where CPMs increased by 4% this month.